If you feel like the “easy” wins in digital subscriptions have vanished, you’re not alone, and the data finally backs you up. The WAN-IFRA World Press Trends Outlook 2025-2026 report reveals an industry at an interesting, if slightly daunting, crossroads.

While the narrative for years has been “digital or bust,” we are now entering a “print + digital + other” paradigm. Digital revenues currently account for 31% of publisher income, but growth has noticeably stalled, nearly matching last year’s figures.

For us at Audiencers, this isn’t a sign to retreat. It’s a signal that the “one size fits all” subscription model is officially broken, that you need to keep innovating, giving audiences more flexibility than ever, whilst building relationships that last.

WAN-IFRA’s Trends Outlook 2026: Subscriptions by the numbers

The shift toward digital continues, but the pace is cooling.

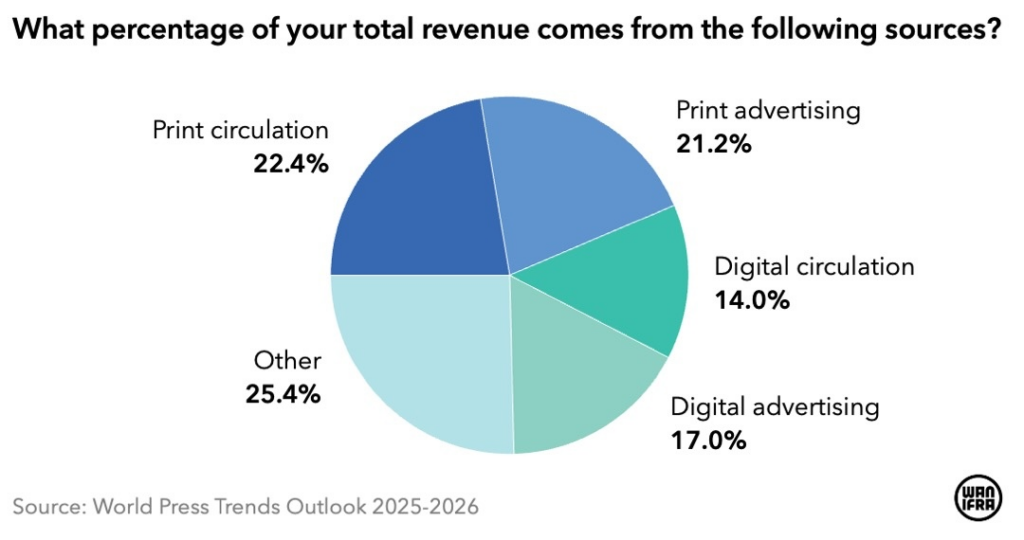

Unlike predictions about print decline over the past years, it remains resilient, and the largest single revenue source.

However, the gap with other income sources is narrowing. Digital circulation now represents 14% of revenue, while income from other activities (events being the greatest part of this, followed by B2B services & e-commerce) lies at an average of 25.4%.

As for reader revenue in particular:

- Digital circulation has grown: from 9% in 2021 to 14% in 2025, a 55.6% increase in under five years

- The adoption gap is closing: 58.5% of news organizations now offer digital subscriptions, a number that jumps to 72.9% in developed markets

- The “Ceiling” effect?: The report suggests that “growth has leveled off and looks to have hit a ceiling… publishers have already signed up many of those prepared to pay” making further acquisition increasingly difficult in a tight economic climate

At Audiencers, we’re less convinced that this “ceiling” has been hit.

In either case, there are some key strategies, many highlighted in the report and across Audiencers, to put in place to combat this “leveled off growth” through a focus towards a more sophisticated and diversified model.

1. Bundling & Family Plans

We’ve seen a significant shift toward high-value bundles over the past few years, combining both national and international brands to reduce the need for a user to pay for multiple subscriptions.

- News Corp brought together three of its best-known publications in October 2025, enabling subscribers of The Australian to also be able to access The Times of London and The Wall Street Journal

- A number of European publishers (Politiken in Denmark, El País in Spain, Italy’s Corriere della Sera and The Irish Times in Ireland) have partnered with The New York Times to offer subscribers access to the NYT’s suite of content

- Le Figaro worked to reduce password sharing, both by limiting simultaneous sessions and developing alternative sharing options, such as Family Packs: “A subscriber to one of these two packages now has the possibility to link 2 to 4 user accounts to their subscription.”

But don’t overcomplicate – as Subscrybe’s Morten Suhr Hansen puts it, “over recent years, many subscription businesses have added layer upon layer: products, pricing models, campaigns, systems, and channels. In 2026, the ability to simplify becomes a competitive advantage. Companies that do not have a clear value proposition, a strong understanding of their core customer segments, and clarity on their key value drivers will struggle – regardless of how much AI they implement.”

> Gain clarity on your purpose with this workshop

> And perfect your value proposition with these 2 frameworks

2. The dynamic paywall

One-size-fits-all is (finally) being left behind for dynamic acquisition models that adapt experiences to a reader’s profile or context. Solutions like Poool, used to put these dynamic strategies in place, are more accessible than ever, built for marketing teams to have autonomy from tech.

What can you adapt to?

- Level of engagement

- Source of traffic

- User status (anonymous, registered, ex-subscriber…)

- Content type / topic

- User location

What can you adapt?

- The type of wall: registration wall, paywall…

- How “tough” the wall is: closable, anti-scroll, full-page, partial-block

- The messaging on the wall

- Introductory offers or pricing proposed

- Currency

A few examples:

- ELLE Magazine’s contextual paywalls, adapted messaging and design to the content type, increased conversion rates by 20%

- Jeune Afrique doubled conversion rates by adapting the paywall messaging and pricing to a user’s level of engagement and location

3. Flexibility and an end to “locking in”

A successful retention model isn’t one that prevents readers from leaving. It’s one where audiences are saved before they even consider cancelling, where unsubscription isn’t the end of the relationship, where alternative, more flexible options exist, and where we accept that people will come and go. Ending the relationship badly doesn’t do us any favors (in fact, it only reduces trust and potentially helps prevent acquisition due to bad past experiences).

What should you do instead?

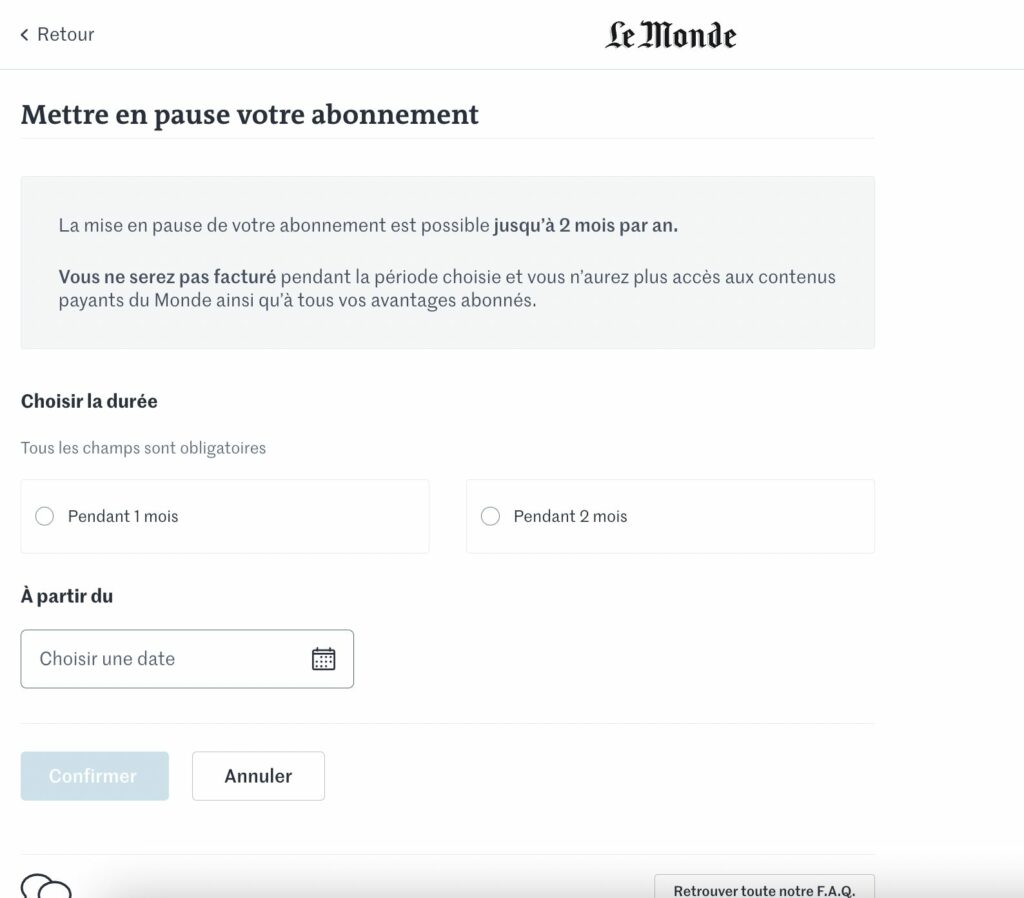

- Pause functionality as a standard: the ability to pause a subscription instead of canceling permanently is an extremely effective retention mechanism. French publisher Le Monde already has this in place

- Easy cancellation is the new retention strategy: simple unsubscription is a necessary foundation for building trust, improving CX, and ultimately turning your pool of ex-subscribers into your biggest future growth opportunity. This is exactly what Nat Geo Kids is proving.

4. Subscriptions as relationships, not contracts

The lines between transactional “subscriptions” and missionary “memberships” are blurring. By developing a community, publishers add an emotional layer to the relationship, making readers more likely to remain loyal and participate thoughtfully.

- Condé Nast has created a “Membership” tier that sits above subscription to build belonging amongst their most loyal audiences. The value exchange here is two-way: members are active participants contributing data, feedback, and engagement. They expect to belong to a community. And the strategy is paying off: a member has an LTV (Lifetime Value) up to 50 times higher than a subscriber, amongst other benefits listed below

- The South African publisher Daily Maverick is perhaps the poster child for these types of membership models, with 40% of its revenues generated by member-driven support. Styli Charalambous, Daily Maverick’s co-founder and CEO told Pugpig in late-2024 that “after three years, 85% of people who start as a member are still there.”

- At The Kyiv Independent, membership means that journalism remains free. With a membership, a reader can support from $5-$100 a month, getting a few benefits in exchange, which have of course evolved over the years. With members based around the world, they’ve worked hard to bring members together, such as through a community map.

- A variety of publishers are creating “clubs” for subscribers, such as DIE ZEIT‘s “Friends of Zeit”, Handelsblatt‘s Circles, The Economist Insider, amongst plenty others.

5. Innovative acquisition channels

Just like revenue streams, acquisition channels are being diversified to reduce reliance on the traditional funnel.

- Referrals at Zetland: Tav Klitgaard, Group CEO and Co-founder, shared how important referrals are for them.

“At Zetland, we have for several years focused on leveraging existing members for acquisition. This is by far the most meaningful way for us to grow, because it builds stronger relationships with both the new members who join through personal recommendations and the existing members who help spread the word about a service that makes a difference in their own lives.

The “contracts” generated by our member-get-member campaigns are far stronger than any ad could ever be.“

- Daily Maverick tackles low conversion rates with a targeted Q&A mailer, significantly enhancing member acquisition and engagement. The initiative addresses the gap between interest and action, providing detailed answers to potential members’ questions, which has led to a notable increase in conversions

- The Times & Sunday Times has been testing an open weekends each year as a way of offering non-subscribers a chance to discover the premium content they have on offer

- Whilst Daily Maverick tested the opposite, proving the importance of their work and helping to finance it

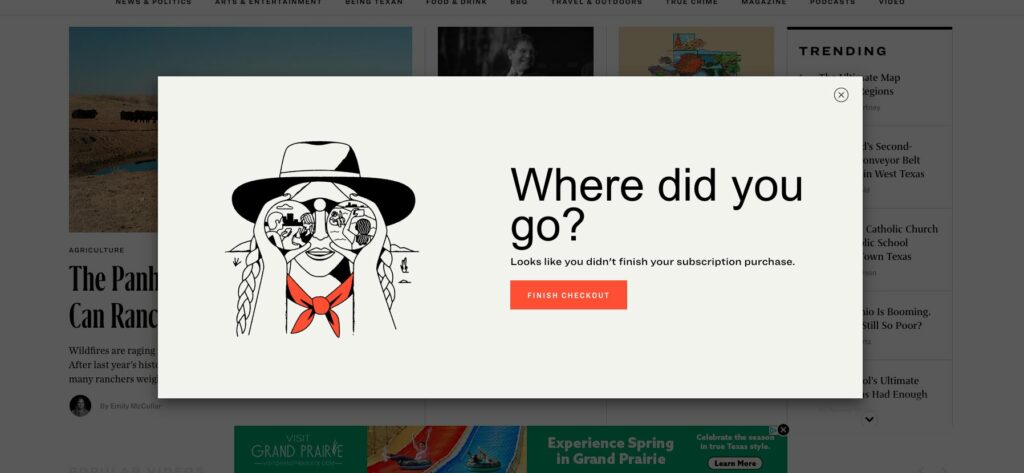

- And learning from other industries such as ecommerce businesses who have abandoned shopping cart notices. The below example from Texas Monthly

> Fancy being inspired by 45 acquisition channel ideas? Well you can, just here.

“Other sources” as the new core?

Perhaps the most shocking finding is the rise of “Other Sources” (events, content services, etc.). This bucket now makes up 25.4% of revenues, almost doubling since 2021.

Events continue to be the main area of activity in this area, with 32.2% of respondents identifying them as an important revenue source, followed by B2B services content and partnerships with platforms (both 16.1%), according to WAN-IFRA’s report.

The secret to building these alternative revenue strategies well? Understanding audience needs, building streams around this and continuously innovating to serve evolving needs.

Panos Sarlanis, Co-founder of IamExpat Media, spoke about this at our 2024 Festival in London.

The question they kept asking: “What essential needs can we solve with new products or services?”

- This led to the launch of directories, helping users find trusted professionals, from tax advisors and language schools to English-speaking dentists, lawyers and career coaches. These have become a significant part of IamExpat’s business model.

- Recognizing the challenges of finding accommodation and employment in new countries, IamExpat also launched a housing platform (aggregating rental properties from partners) and a job board specifically tailored for their international and multilingual audience.

These “classifieds”—directories, housing, and job boards—now account for a considerable part of their revenue. Directories contribute the most, and this highlights the high value and conversion rate of these specialized services that focus on user needs.

The direction is clear: To succeed in 2026, you can’t rely on content access alone. Publishers should build an ecosystem with the audience at the center, where subscription is the gateway to a community, not just a library of text.